Share This Article

India’s Income Tax Act, 1961 survived over 60 Finance Acts and more than 4,000 individual amendments across six decades before the government decided enough was enough.

The Income Tax Act, 2025 — passed by both Houses of Parliament in the monsoon session of 2025 — takes effect from April 1, 2026. It replaces the 1961 Act not with new tax rates or a new tax structure, but with a rebuilt version of the same law: cleaner language, logical sequencing, fewer redundant provisions, and a significantly more detailed data collection framework.

For most taxpayers, the rates stay the same. For tenants specifically, the changes in how HRA is claimed are meaningful — and immediate.

Table of Contents

What the New Act Changes — Overview {#overview}

The Income Tax Act 2025 contains 536 sections and 16 schedules — compared to 819 sections and 14 schedules in the 1961 Act. The reduction in section count reflects the removal of redundant provisions and the consolidation of related sections — not a reduction in the scope of taxation.

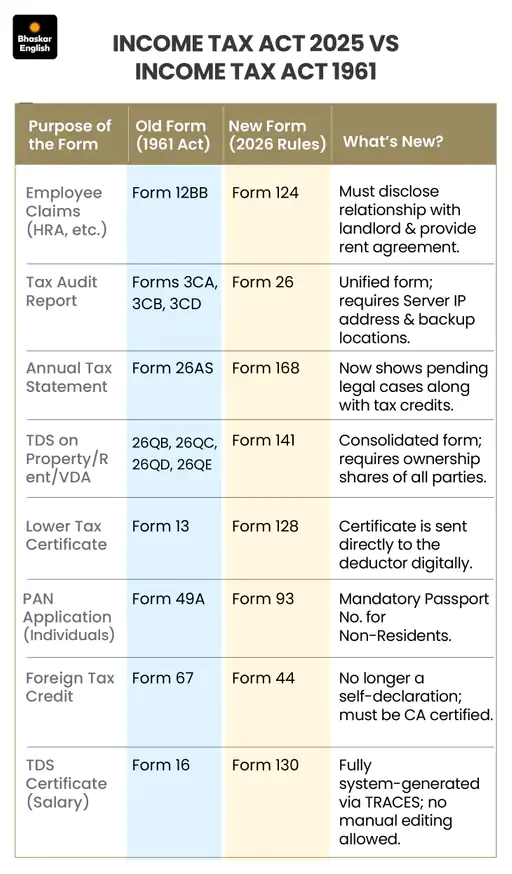

All TDS provisions that previously ran from Sections 192 to 194T across more than 60 separate sections have been consolidated into three sections under the new Act. Section 392 covers salary TDS. Section 393 covers TDS across structured tables for residents, non-residents, and all persons.

According to CA Ashish Niraj, Partner at A S N & Company, the new system is heavily focused on monetary data collection. “The goal is to ensure the Income Tax Department has a complete digital map of a taxpayer’s life before they even file the ITR,” he said.

[INCOME TAX COMPARISON IMAGE PLACEHOLDER]

The Biggest Change for Tenants: Form 124 and HRA {#hra-change}

[IMAGE BLOCK 2 — Mid-article]

The old Form 12BB — used by employees to declare deductions including HRA — has been replaced by Form 124 under the new Act.

The change is not just cosmetic. Form 124 requires significantly more information than its predecessor.

Previously, claiming HRA required submitting your rent amount, your landlord’s name, and their PAN (if annual rent exceeded ?1 lakh). Form 124 now additionally requires:

- Your relationship with the landlord — a new disclosure requirement

- A copy of the rent agreement itself — not just the details, but the document

This is a targeted change aimed at a specific practice: employees claiming HRA by paying rent to a family member — typically a spouse or parent — who does not report that rental income in their own returns.

As CA Niraj put it: “Many people who pay rent to family members will now be on the government’s radar. The IT Department will easily check if the person receiving that rent is actually reporting it as income in their own tax filings.”

Paying Rent to Family Members — Now Under Scrutiny {#family-rent}

This disclosure requirement has direct implications for two categories of taxpayers:

Paying rent to parents: This practice has long been a legitimate tax-saving mechanism — provided the rent is genuine, reasonable, the property is actually owned by the parent, and the parent declares it as rental income. Under Form 124, the relationship disclosure ensures the IT Department can cross-verify both sides of this transaction digitally.

If the parent is reporting the rental income correctly, this change is administrative — it creates a verifiable link but does not change the legitimacy of the arrangement.

Paying rent to a spouse: This has already been consistently rejected by Indian tax courts and the Income Tax Appellate Tribunal as a circular transaction. Form 124 makes this easier to identify and challenge.

The practical guidance remains unchanged: rent paid to parents, where genuine and correctly reported, is valid. Rent paid to a spouse is not.

Related read: Rent receipt for HRA — 5 rules that could save or cost you taxes ?

The New PAN and NRI Rules {#pan-nri}

The process of applying for a Permanent Account Number is also changing. The old Form 49A is replaced by Forms 93 to 96, depending on the applicant’s profile.

For non-residents: providing a passport number is now mandatory.

For global taxpayers: a Tax Identification Number from the country of residence must be provided.

These changes are part of the broader data-mapping initiative. The IT Department is building a more complete picture of taxpayer identity — particularly for individuals with cross-border income or assets.

Property Deals and Multi-Owner Disclosure {#property-deals}

Form 141 replaces several older forms including Form 26QB, used for TDS on property transactions. The new form requires, when a property has multiple owners or multiple parties involved, the exact shareholding percentage of every buyer, seller, landlord, and tenant involved in the transaction.

This directly affects joint property arrangements — common in Indian families — and co-tenancy situations where multiple tenants share a rental.

Form 168 replaces the familiar Form 26AS — the annual tax credit statement that taxpayers use to verify TDS deducted and deposited against their PAN.

What the “Tax Year” Change Means {#tax-year}

One of the most visible structural changes in the new Act is the replacement of “Previous Year” and “Assessment Year” with a single concept: the Tax Year.

Under the 1961 Act, income earned in the “Previous Year” (e.g., FY 2023–24) was assessed in the “Assessment Year” (AY 2024–25). The two-label system was a persistent source of confusion, particularly in client communications and return forms.

The 2025 Act replaces both with a single Tax Year running from April 1 to March 31. Income earned in Tax Year 2026–27 is assessed for Tax Year 2026–27 — no separate Assessment Year label.

This applies from April 1, 2026. Income earned before that date is still governed by the 1961 Act.

What Tenants Should Do Now {#what-to-do}

If you claim HRA: Prepare to submit Form 124 with your employer’s HR or accounts team during the next declaration cycle. Have your rent agreement ready as a document — not just the details. Know your relationship with your landlord and be prepared to state it.

If you pay rent to parents: Verify that your parent is correctly declaring the rental income in their own ITR. Cross-verification is now structurally easier for the IT Department. A mismatch will attract scrutiny.

If you pay rent to a spouse: Stop claiming HRA on that basis. The practice has never been legally valid, and Form 124 makes it significantly more visible.

If your annual rent exceeds ?1 lakh: Your landlord’s PAN remains mandatory. Combined with the rent agreement submission requirement under Form 124, having a properly drafted and signed agreement is now not just a legal protection — it is a tax document requirement.

The official Income Tax India portal has FAQs and transition guidance for the new Act.

Final Thought

The Income Tax Act 2025 is not a new tax. It is a rebuilt version of an old one — with better language, consolidated provisions, and a significantly more detailed data architecture.

For tenants, the core takeaway is this: the rent agreement that you signed is now a tax document as well as a legal one. Form 124 asks for it. The IT Department will use it to verify your HRA claim and cross-check your landlord’s income declarations.

That agreement you signed — or didn’t bother to get signed properly — now has another layer of consequence.

Understand HRA rules fully before your next claim. Read our HRA and rent receipt guide ?